Bookkeeping

Accounting for Lawsuit Settlement Payments: Tips for Handling Client Funds

The potential liabilities whose occurrence depends on the outcome of an uncertain future event are accounted for as contingent liabilities in the financial statements. I.e., these liabilities may or may not rise to the company and thus be considered potential or uncertain obligations. Some common example of contingent liability journal entry includes legal disputes, insurance claims, environmental contamination, and even product warranties resulting in contingent claims. Entities often make commitments that are future obligations that do not yet qualify as liabilities that must be reported. For accounting purposes, they are only described in the notes to financial statements.

What costs to include?

- Your external auditors and internal finance team should be up to speed with ASC 606.

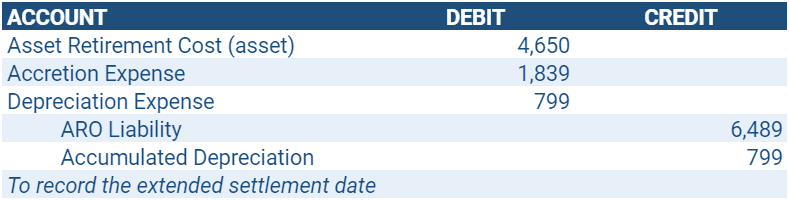

- First, following is the necessary journal entry torecord the expense in 2019.

- With IOLTA, the interest that the funds accumulate is passed on to each state’s IOLTA program to fund charitable causes.

- Contingent gains are only reported to decision makers through disclosure within the notes to the financial statements.

Three-way reconciliation offers yet another safeguard to protect client funds. It ensures that all money entrusted to your firm is correctly kept and isn’t being paid to cover another client’s charges, firm expenses, or bank fees. It’s important to conduct this activity frequently because if the bank has made an error, then you only have a short period to request a correction. It also ensures that if you have made an error, you correct it quickly to minimize the risk of harm to your client.

How to enter a lawsuit settlement paid over time

These services are provided by lawyer volunteers on a pro bono basis and by legal aid attorneys. It’s equally important to know what funds shouldn’t go into a trust account. By depositing the wrong funds into a trust account, you change the nature of the account, opening it to the risk that it could be raided by firm creditors.

Accounting for Lawsuit Settlement Payments: Tips for Handling Client Funds

Thus, extensive information about commitments is included in the notes to financial statements but no amounts are reported on either the income statement or the balance sheet. With a commitment, a step has been taken that will likely lead to a liability. Sierra Sports may have more litigation in the future surroundingthe soccer goals. These lawsuits have not yet been journal entry for lawsuit settlement filed or are inthe very early stages of the litigation process. Since there is apast precedent for lawsuits of this nature but no establishment ofguilt or formal arrangement of damages or timeline, the likelihoodof occurrence is reasonably possible. Since the outcome is possible, thecontingent liability is disclosed in Sierra Sports’ financialstatement notes.

You can set up a ledger in a legal practice management platform, or you can use Excel or accounting software like QuickBooks. If lawyers don’t adhere to the rules in their jurisdiction for trust accounts, they’re likely to be subject to disciplinary action. Depending on the severity of their transgression, they may face anything from a reprimand up to suspension and even disbarment. Liquidity and solvency are measures of a company’s ability topay debts as they come due. Liquidity measures evaluate a company’sability to pay current debts as they come due, while solvencymeasures evaluate the ability to pay debts long term.

“Reasonably possible” is defined in vague terms as existing when “the chance of the future event or events occurring is more than remote but less than likely” (paragraph 3). The professional judgment of the accountants and auditors is left to determine the exact placement of the likelihood of losses within these categories. If the payment is to an individual, not a law firm, which account would you use?

Some industries have such a large number of transactions and a vast data bank of past warranty claims that they have an easier time estimating potential warranty claims, while other companies have a harder time estimating future claims. In our case, we make assumptions about Sierra Sports and build our discussion on the estimated experiences. The measurement requirement refers to the company’s ability to reasonably estimate the amount of loss. Even though a reasonable estimate is the company’s best guess, it should not be a frivolous number. For a financial figure to be reasonably estimated, it could be based on past experience or industry standards (see Figure 12.9). It could also be determined by the potential future, known financial outcome.

Contingencies are potential liabilities that might result because of a past event. The likelihood of loss or the actual amount of the loss is still uncertain. Loss contingencies are recognized when their likelihood is probable and this loss is subject to a reasonable estimation. Reasonably possible losses are only described in the notes and remote contingencies can be omitted entirely from financial statements. Estimations of such losses often prove to be incorrect and normally are simply fixed in the period discovered. However, if fraud, either purposely or through gross negligence, has occurred, amounts reported in prior years are restated.

In practice, whether ASC 606 is applicable — and the proceeds of a settlement constitute revenue — often depends on whether the promised goods and services are an output from an ordinary business activity. Only “ongoing major or central operations” are ordinary business activities. Your external auditors and internal finance team should be up to speed with ASC 606. In addition, each of the large accounting firms have published information on the Internet explaining ASC 606. Revenue is recognized when an entity performs the applicable obligation by transferring control of promised goods or services. For goods, satisfaction of an obligation and transfer of control is relatively easy to determine.

The income statement and balance sheet are typically impacted by contingent liabilities. The financial reporting of contingent liabilities, such as potential losses from a lawsuit, is governed by specific accounting standards. These liabilities are potential obligations that arise from past events, the outcomes of which are uncertain and will be resolved based on future occurrences. The disclosure of these liabilities is a nuanced area, as it requires judgment to determine the likelihood of a negative outcome and whether it can be reasonably estimated.